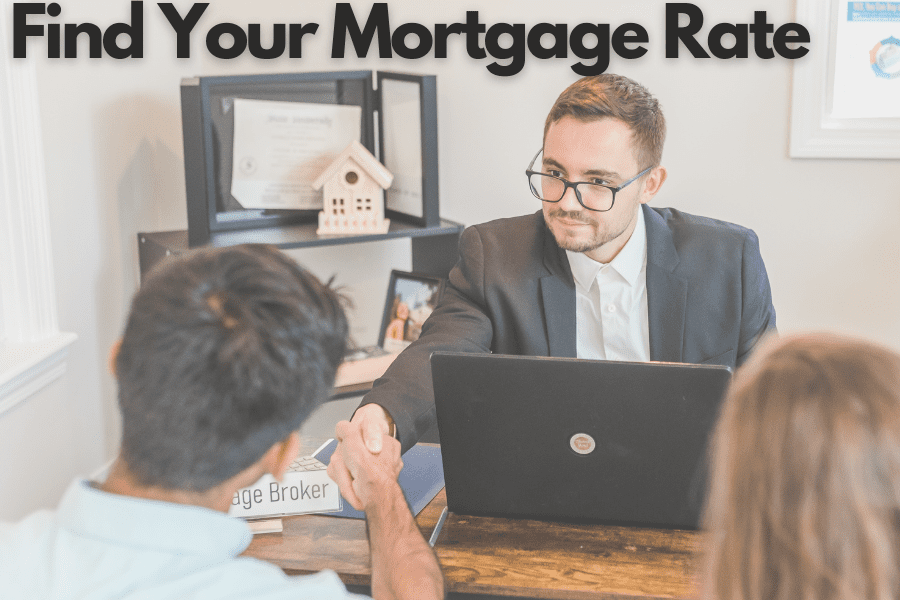

There are certain times in life when we need finances urgently. In similar situations, being a homeowner proves to be a boon as you can mortgage your home for the required finances. The advantage of a Mortgage Rate is that you do not have to leave your power over the property and can get the loan at veritably low-interest rates as compared to other loans. However, for that, you need to know about mortgage loans.

A Mortgage loan is simply a loan taken out against a property you live in. The property in question could be your house, a shop, or a non-agricultural piece of land. The lender provides you with the top loan amount and charges you interest on it. You can repay the loan in affordable yearly installments. Similarly, the lender has a legal claim over the property for the term of the loan, and if the borrower defaults in paying off the loan, the lender can seize it and auction it off.

Understand About Mortgage Loan and Mortgage Rate:

-

Fixed-Rate Loan Benefits

Best Mortgage Rates are designed to cover borrowers from unexpected and constantly considerable increases in their yearly mortgage payments if interest rates rise. They are easy to understand and do not change much from lender to lender. They are frequently ideal for everyone from first-time buyers to those looking at investment properties.

-

Downsides to Fixed-Rate Loans

One of the disadvantages of fixed-rate mortgages is the qualifying criteria that homeowners must meet. For example, if interest rates are high, it can make qualifying for this type of loan much more delicate because the payments will be less affordable for some people.

-

Protection Against Interest Rate Increases

If interest rates rise — or indeed double or triple — you still reap the benefits of the low-interest rate that you locked in at the launch of your loan. Although Best Mortgage deals generally have several caps that determine how important your interest rate can rise, for numerous borrowers, a rate hike of many chance points can be burdensome.

-

Home location

Numerous lenders offer slightly different interest rates depending on what state you live in. One may looking for most accurate rates using the Interest Rates tool. All you need to verify your state, depending on your loan amount and loan type.

Still, our website will help you get a sense of the mortgage rates available to you, but you will want to safeguard around with multiple lenders if looking to buy in a rural area. Lending institutions, according to their requirement, can offer different loan rates. Regardless of whether you are looking to buy in a rural or metro area, talking to multiple lenders will help you understand all of the options available to you. It is a must to go through a Mortgage Comparison of different deals.

-

Need To Understand!

If you pay a high-interest rate, the lender gives you money to neutralize your closing costs. When you accept lender credits, you have to pay lower upfront. Keep in mind that some lenders may also offer lender credits that are unconnected to the interest rate you pay. This For illustration, a temporary offer, or to compensate for a problem.

Final Words

A mortgage rate is generally for people who anticipate declining interest rates. They plan to live in a particular home many times. They also anticipate paying off their mortgages before the interest rate acclimation period. These homebuyers must also have the disposable income to make high mortgage payments to stay longer in the home, and interest rates rise.

Are you require funds and are looking to borrow money against your home? Choose safety and get in touch with 1st Choice Mortgages, which Provides the Best Mortgage Deals.

{kind=link}